(recent exacerbation of an old problem)

Bankruptcy/CGT liability

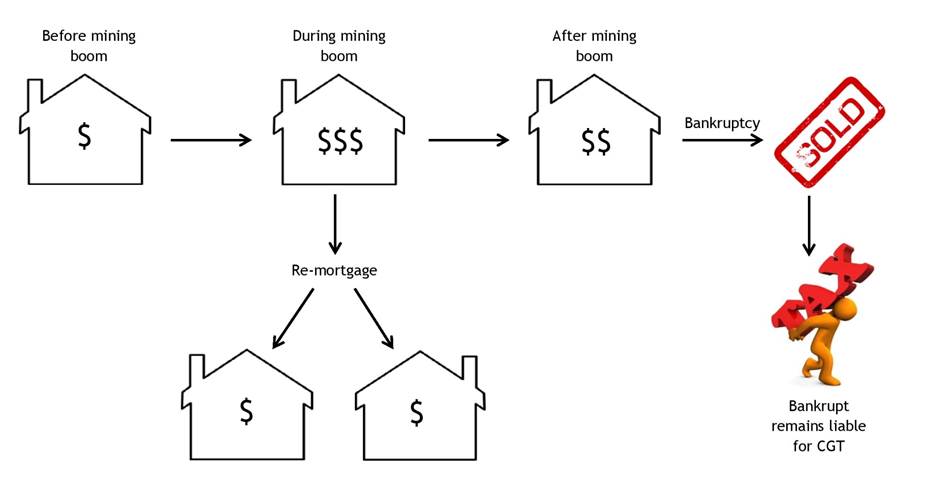

An individual can face a second bankruptcy as a result of a first bankruptcy that involves an investment property or other CGT assets.

An individual’s CGT asset vests in a trustee because of the bankruptcy of the individual. However, no CGT event happens as a result of the vesting.

An individual’s CGT asset vests in a trustee because of the bankruptcy of the individual. However, no CGT event happens as a result of the vesting.

If the trustee later sells the CGT asset (e.g. an investment property) and a capital gain (or loss) arises, it is a capital gain (or loss) made by the individual, and not the trustee. In other words, although the trustee is selling the asset in a bankruptcy scenario, any resulting CGT liability remains with the bankrupt personally, and not with the trustee.

The ATO relies on Section 106.30 of the Income Tax Assessment Act 1997 for its view on this outcome in personal insolvencies.

The bankrupt’s liability for any CGT is borne by the bankrupt in the year of income in which the disposal occurs.

Therefore, if the bankruptcy trustee realises a large capital gain from the sale of a bankrupt’s real property or shares, that money is applied to pay out creditors. The bankrupt does not receive any of the capital gain but is personally liable for the resulting income tax. This may necessitate a second bankruptcy to address that liability.

This outcome is in contrast to a corporate insolvency context where if a liquidator sells a CGT asset of a company, any capital gain (or loss) is made by the company but it is the liquidator who is responsible for payment of the CGT liability.

We at Sheridans have found that this issue has come to prominence again in recent times as we have been approached by individuals with property portfolios in the north-west of Western Australia, particularly those who have held the properties for some time, remortgaged the properties as they increased in value in order to acquire additional properties, only to then see property prices and income decrease in the last few years. Notwithstanding these individuals are in financial difficulty, there is the potential for capital gains when the properties are sold.

This issue appears to be another example of an impediment to the “fresh start” objective that the bankruptcy legislators often refer to.

A further example is the issue of the “after-acquired property” rules contained in the Bankruptcy Act (see Sheridans’ View Issues 31 (April 2015) and 32 (July 2015)).

One way to resolve the CGT issue is for the bankrupt to sell their CGT assets prior to bankruptcy but unfortunately this is not always possible.

April 2017