Debt agreements are at an all time high.

Figures released by AFSA for the March quarter 2017 show that debt agreements are the highest on record at 3,584 for the quarter. Debt agreements reached record highs in Western Australia, Victoria, Queensland and South Australia.

At the same time, we have seen the burgeoning of debt management businesses, with their heavy and sustained advertising and promotion on day-time and late-night television, and through prominent websites and internet advertising.

Make a quick phone call to get debt free, so you

can get on with living a stress-free life.

The record high level of debt agreements and the proliferation of debt management businesses is obviously not unrelated.

Debt agreements are being strongly promoted and recommended by these debt management businesses and there is considerable concern about this development.

The disquiet in the insolvency industry and with consumer and community advisors, and regulators (AFSA and ASIC), concerns the apparently indiscriminate and sometimes ill-advised use of the debt agreement.

Debt agreements are being promoted as an alternative to bankruptcy and often extremely optimistic views are promoted to vulnerable people in financial distress about what can be achieved through a debt agreement.

What is generally left unsaid is that practically speaking the consequences of entering a debt agreement can be very similar to bankruptcy.

As a result, while debt agreements can suit some people, they are not appropriate for others, and bankruptcy may indeed be the better option.

I recommend the Consumer Action Law Centre’s Media Releases regarding debt agreements for commentary on the concerns regarding debt agreements and debt management businesses (www.consumeraction.org.au).

But why this proliferation of advisors and surge in debt agreements?

Obviously a contributing factor was the earlier economic downturn in the eastern states, which has more recently been followed in Western Australia with the downturn in the state’s vital mining sector.

But in my opinion there has been a second important contributing factor: the steady and relatively dramatic increase in the eligibility threshold limits for debt agreements.

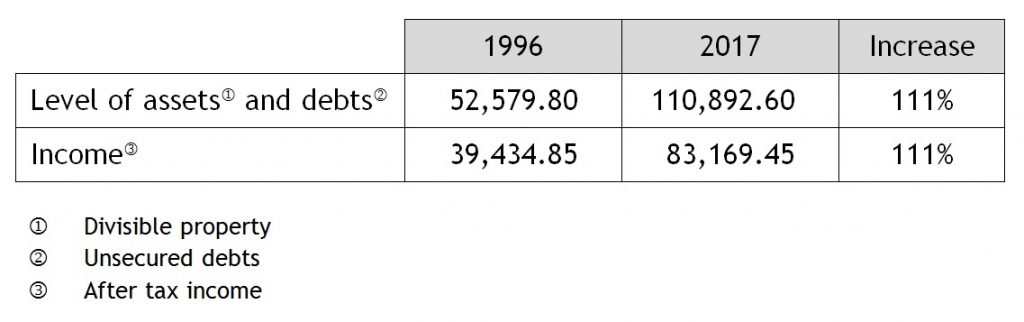

Debt agreements, which are regulated by the Bankruptcy Act, were introduced in 1996.

The eligibility threshold limits then and now are as follows:

Therefore the increase in debt agreements’ eligibility threshold limits has outstripped, or increased faster than, the CPI increase.

In the same period (1996 to 2017) the consumer price index (CPI) has increased by 67%.

I do not know why this has happened and whether there was some strategic reasoning behind it.

However, the clear consequence is that more people in financial difficulty are eligible for debt agreements.

For debt management businesses it has produced a bigger, more lucrative market of potential clients in financial distress, a market that is generally less sophisticated and knowledgeable than the business community, and which is therefore more malleable and susceptible to manipulation.

The regulators are monitoring this segment of the insolvency market. Last Monday, 29 May 2017, AFSA released a new video entitled “Bankruptcy Advice: Untrustworthy Advisors” for consumers which “explains in simple terms how easy it is for consumers to be tricked into taking untrustworthy advice from unregulated, unlicensed advisors who may target vulnerable people in times of financial crisis and pressure”. The video is the result of collaboration between AFSA, ASIC and ARITA.